- November 3, 2025

- by k2recyclers

- E-Waste News

- 274 Views

- 0 Comments

The Growing Tide of Electronic Waste

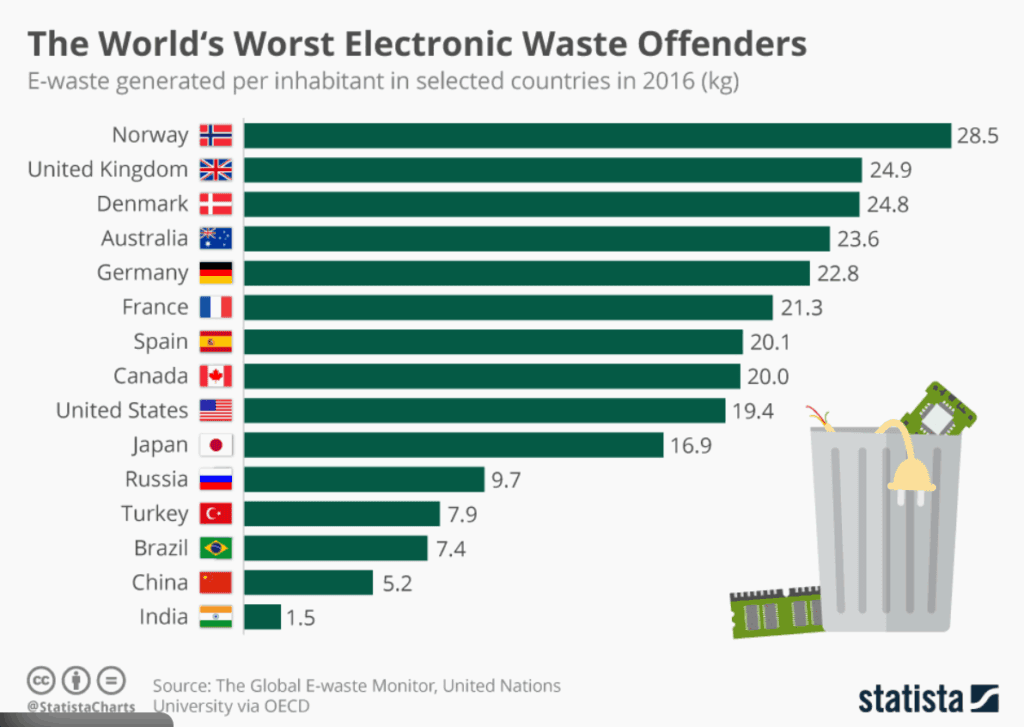

According to United Nations Institute for Training and Research/International Telecommunication Union, global e-waste generation reached about 62 million tonnes in 2022, up ~82 % compared to 2010.

Alarmingly, less than ~22.3 % of that was formally collected and recycled.

The reason the volume keeps growing: shorter electronics lifecycles, more devices per person, and more device types (smartphones, wearables, IoT, data-centres).

In India, for example, formal e-waste processing is increasing in some states but remains inconsistent.

Policies & Regulatory Shifts

In India, the government has launched a Rs 1,500 crore incentive scheme under the Ministry of Mines to boost the recycling of critical minerals from e-waste and used batteries.

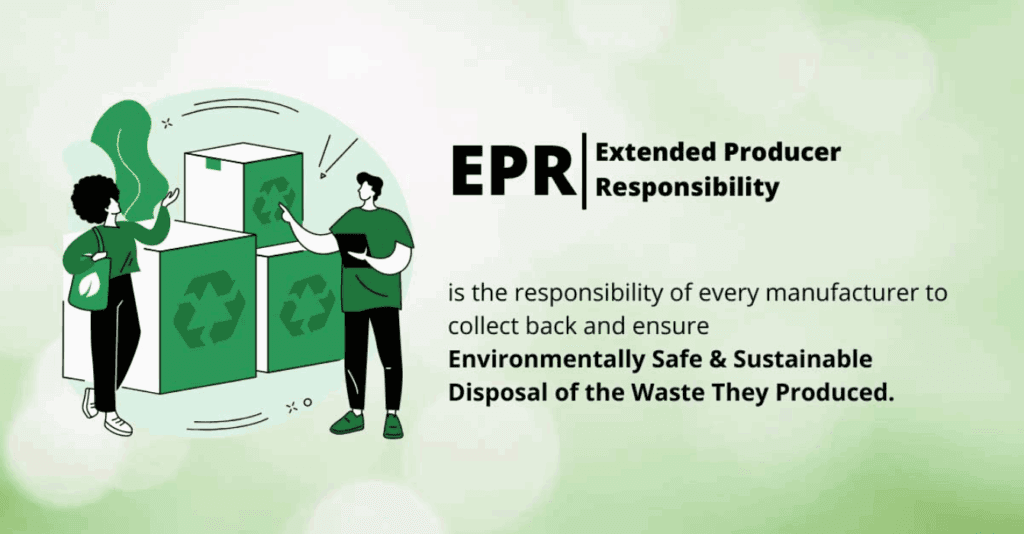

The concept of Extended Producer Responsibility (EPR) is gaining traction: manufacturers are increasingly being made responsible for the end-of-life of their electronics.

In major markets, the collection infrastructure, take-back rules, and certification of recyclers are being strengthened.

Some brands and manufacturers are pushing back / challenging regulatory changes: e.g., lawsuits in India from electronics giants over new e-waste rules.

The sheer growth of e-waste is outpacing the development of recycling infrastructure, prompting regulatory attention.

Technology & Automation in Recycling

Robotics, AI, sensors, and automated sorting are increasingly being used in recycling operations. For instance, in Denmark, a robotic system is being developed to disassemble laptop screens as part of e-waste recycling.

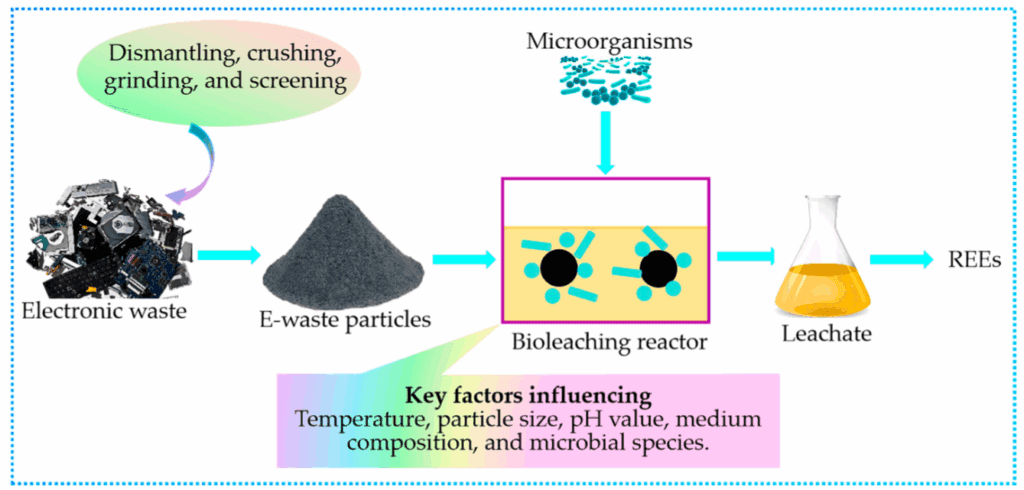

Researchers at ETH Zurich have developed a new extractant to recover rare earth elements (REEs) from e-waste (which historically have been extremely challenging to recover).

Trend reports suggest that by 2025, we should see automation such as AI‐powered sorting achieving very high accuracy, and emerging processes like plasma-arc recovery and advanced chemical / ionic-liquid recovery.

Example: A US waste‐management company (“Waste Management Inc.”) is investing in a $3 billion tech-driven recycling push with smart facilities, indicating the investment scale of the shift.

Recovery of Critical & Rare Materials

Many electronics contain small but highly valuable or strategically important materials—like tantalum (in capacitors), lithium, cobalt, and rare earths. A recent article noted that tantalum is widely present in our devices and yet largely lost in landfills.

As mentioned, the ETH Zurich team is pioneering methods to more efficiently separate rare earths from e-waste.

In India, the incentive scheme explicitly targets recycling of e-waste + used lithium-ion batteries to reduce reliance on imports.

Market Growth & Investment

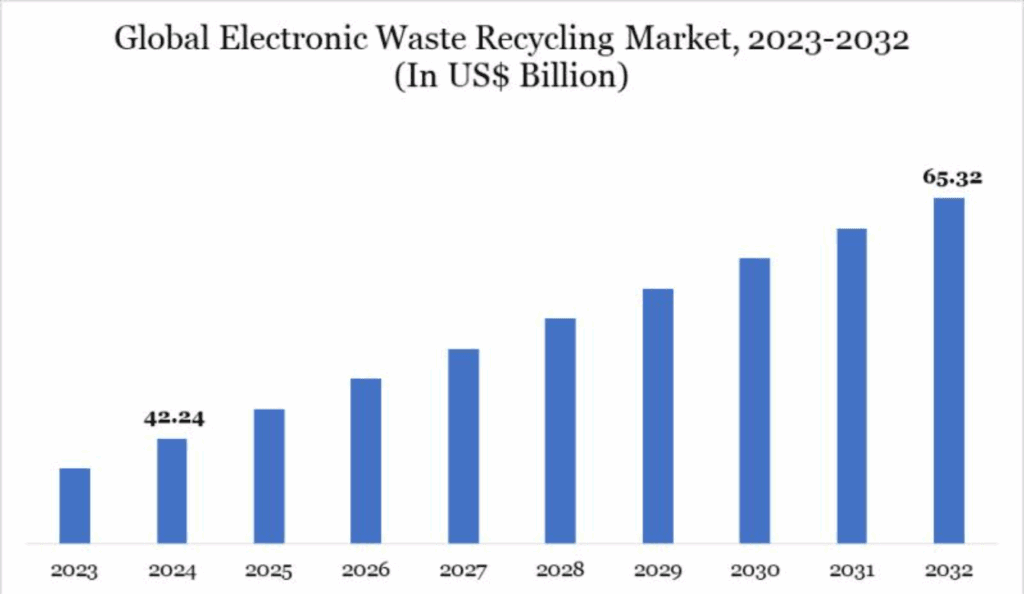

Several market reports cite strong growth: e.g., the global e-waste management market is projected to grow from ~USD 77.99 billion (2024) to ~USD 259.5 billion by 2032 (CAGR ~16.24 %).

Some other reports project slower growth (~CAGR 7.4 %) depending on region and scope.

More infrastructure, collection systems, and investment (in both developed and emerging markets) are being announced.

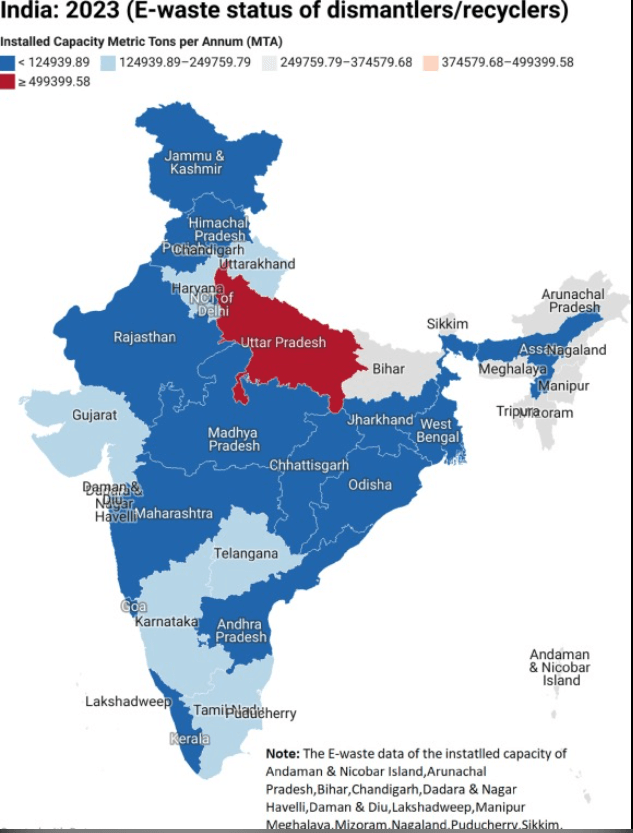

Regional Spotlight – India

Government data shows some Indian states making big gains in e-waste processing: e.g., Uttar Pradesh increased from ~236,727 mt to ~388,160 mt; Haryana from ~110,062 mt to ~149,654 mt.

But many states show negligible or declining figures, highlighting infrastructure and formalization gaps.

Experts in India are calling for policy frameworks to support formal recycling and strengthen the circular economy in electronics.

Consumer-take-back platforms are being launched: e.g., Attero Recycling’s “Selsmart” platform in India allows consumers to book e-waste pickup and ensures responsible data wiping + recycling.

Challenges & Hurdles

The informal sector remains dominant in many countries (especially developing ones) for e-waste collection/recycling — leading to safety, health, and environmental issues.

Though the generation of e-waste is increasing fast, the rate of formal collection & recycling is lagging significantly.

Complex device composition and rapid technology change make recycling difficult (many device types, multi-materials, precious components). The variance makes automation tough.

Cost pressures: recovering some rare materials or disassembling complex electronics is still expensive vs landfill or export.

For India: some states have weak formal infrastructure; drop-off systems may be inadequate; consumer awareness may be low.