- November 13, 2025

- by k2recyclers

- Metal News

- 261 Views

- 0 Comments

The Metal Momentum

The metal and steel industry in 2025 is navigating a confluence of domestic growth, trade policy shifts, sustainability demands, and global structural pressures. For recycling and secondary‐metal businesses, this is a moment of opportunity—but also of responsibility. Success will go to those who can source and process quality materials, adapt to changing trade and quality norms, align with sustainability goals, and strategically integrate into the broader metal value chain.

Price & Non-Ferrous Metals Trends

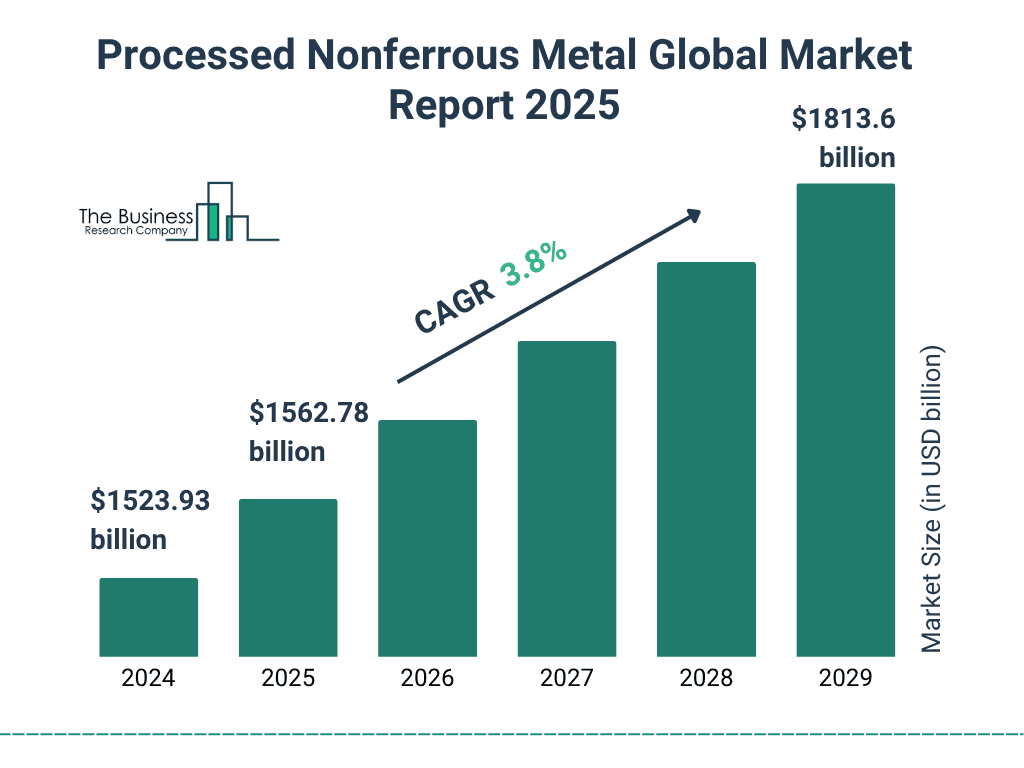

Prices of key non-ferrous metals—such as copper, aluminium, and zinc—are seeing upward pressure. For example, in India, the demand for non-ferrous metals grew ~9% year-on-year, driven by infrastructure, electrical, and renewables rollout.

This createsan opportunity for metal recyclers and secondary-metal supply chains: a higher value of recovered metals means stronger economics for scrap collection & processing.

Steel Sector: Domestic Indian Context

India is among the few countries showing growth in crude steel and DRI (direct-reduced iron). In January-March 2025, India’s DRI output was 14.186 MnT (up 6.3% YoY), accounting for ~49.2% of global DRI production in that period.

Domestic steelmakers continue to flag the problem of cheap imports, especially from China and other countries, which are affecting capacity utilisation and profitability.

The government is implementing schemes to promote low-carbon / “green steel” technologies. For example, a scheme under India’s Ministry of Steel (worth several ₹ thousand crores) to promote clean-steel production.

These dynamics suggest that for anyone in the metal business—including scrap, secondary steel, or recycling—there’s a strong signal: focus on quality feedstock, efficiency, and alignment with decarbonisation trends.

Global Industry Trends & Challenges

According to a 2025-2026 sector outlook report, the global metals and steel industry faces several headwinds: oversupply (especially from China), tariff/ trade barriers, and the high cost of transitioning to greener technologies (e.g., electric arc furnaces, scrap-based steel making).

For example:

Basic metals growth globally is forecasted to be around just 2.2% in 2025, dropping to 0.7% in 2026.

New steel-making capacity expansion is significant: up to ~165 million metric tonnes planned from 2025-2027, mostly in Asia (58% of new capacity).

Regions like Europe are under pressure due to high energy costs, lower demand, and trade/tariff actions.

For players in India/NCR region, this means: take advantage of domestic demand growth, but be mindful of global cost pressures, energy/efficiency demands, and potential trade/tariff risk.

Trade Policy and Imports/Exports – Key Moves

In India, steel makers gained some positive momentum when a government body recommended a temporary ~12% tax on certain steel imports (for 200 days) to curb cheap product imports.

In aluminium, the Aluminium Association of India (AAI) recently requested the government to raise import duties to 15% and enforce stricter scrap-quality norms, to protect domestic producers from imports & dumping.

On the global front, the European Union proposed halving its tariff-free quota for steel imports and post that implementing a 50 % tariff on further imports, including those from India.

Sustainability, Circular Economy & Diversity in Operations

The metal industry is moving—not just on volume—but on the sustainability agenda. For example, higher demand for “green steel” (lower-carbon production routes) offers a window for recyclers who can supply high-quality scrap and feedstock that supports these routes.

In India, Hindustan Zinc (HZL) opened night shifts for women engineers at its Debari smelter, signalling increasing focus on diversity and inclusive operations in the metals sector.

For a recycling/metal business, this means: aligning with ESG (environment, social, governance) trends is becoming not optional—it’s integral. Being able to show safe, inclusive operations and high-quality, traceable scrap inputs will be a differentiator.

The Recycling Ripple Effect

These trade policy shifts matter for the recycling industry because:

Demand-side shifts (tariffs, quotas) impact what metals are imported/exported, and thus affect scrap supply/demand dynamics.

Quality standards and scrap norms (like the AAI case) directly affect the kind of scrap feedstock that is acceptable.

Export/import policy may create arbitrage opportunities (or challenges) for recovered metals.